Great Strong Suggestions About Residence Mortgages That Anybody Can Use

Written by-Flanagan SantanaHave you been searching for a home mortgage but feel overwhelmed at all the information that is out there? Don't worry, the following article will get you caught up on all the necessary information you must know when applying for a home mortgage. Even if you aren't looking for a mortgage now, anyone can get valuable information by continuing to the article below.

Before attempting to secure a loan, you should take the time to look over your credit report, as well as making sure that your financial situation is in perfect order. Credit standards are becoming even more strict, so work on your credit as soon as possible.

Be prepared before obtaining your mortgage. Every lender will request certain documents when applying for a mortgage. Do not wait until they ask for it. Have the documents ready when you enter their office. You should have your last two pay stubs, bank statements, income-tax returns, and W-2s. Save all of these documents and any others that the lender needs in an electronic format, so that you are able to easily resend them if they get lost.

Refrain from spending excessively while you wait for your pre-approved mortgage to close. If a lender notices lots of charging activity before your mortgage is a done deal, they could change their mind about lending to you. Once you've signed the contract, then you can spend more.

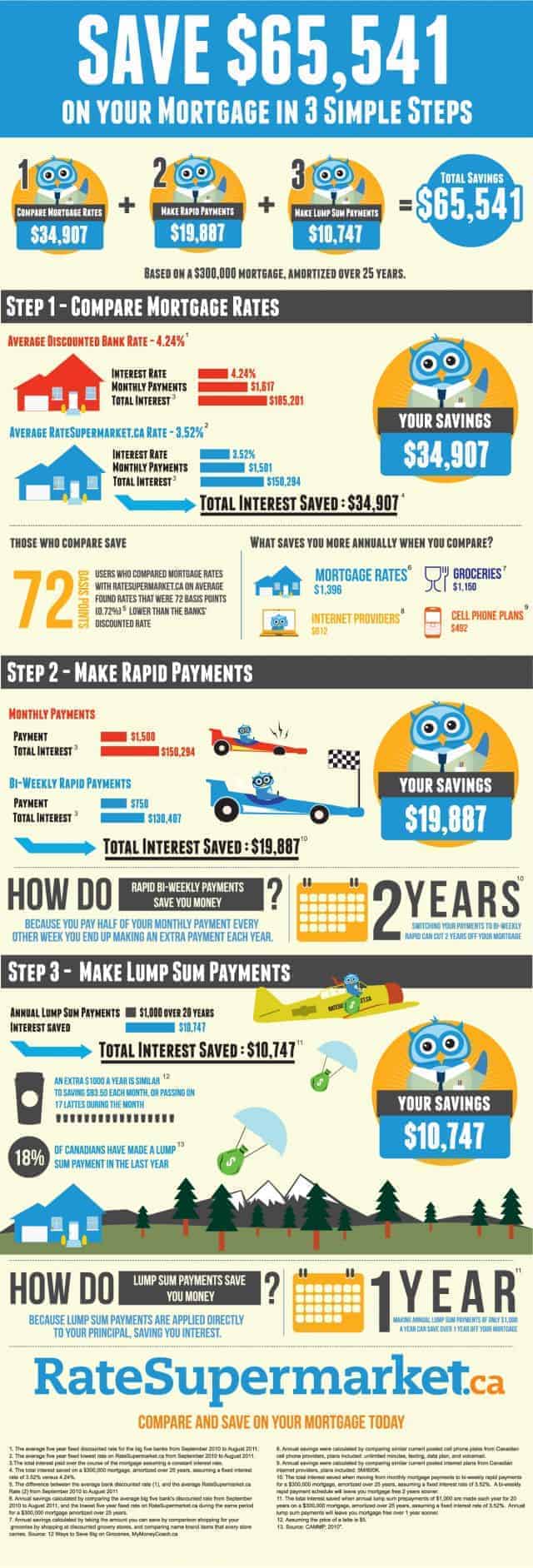

When you see a loan with a low rate, be sure that you know how much the fees are. Usually, the lower the interest rate, the higher the points. These are fees that you have to pay out-of-pocket when you close your loan. So, be aware of that so you will not be caught be surprise.

Understand the difference between a mortgage broker and a mortgage lender. There is an important distinction that you need to be aware of so you can make the best choice for your situation. A mortgage broker is a middle man, who helps you shop for loans from several different lenders. A mortgage lender is the direct source for a loan.

Look into no closing cost options. If closing costs are concerning you, there are many offers out there where those costs are taken care of by the lender. The lender then charges you slightly more in your interest rate to make up for the difference. This can help you if immediate cash is an issue.

Put as much as you can toward a down payment. Twenty percent is a typical down payment, but put down more if possible. Why? The more you can pay now, the less you'll owe your lender and the lower your interest rate on the remaining debt will be. It can save you thousands of dollars.

Try giving your lender a chance to help you with mortgage payment problems. If you struggle to make payments, do not ignore your lender's services. There are various new programs to help you keep up with your mortgage payments like forbearance if you have an FHA mortgage. Lenders are generally happy to work out any delinquent loans via loan modifications, or possibly short sales if you can't afford to keep your home. It can be difficult to deal with them over this, but communication is key.

Lenders look at your debt-to-income ratio in order to determine if you qualify for a loan. If your total debt is over a certain percentage of your income, you may have trouble qualifying for a loan. Therefore, reduce your debt by paying off your credit cards as much as you can.

If you are a retired person in the process of getting a mortgage, get a 30 year fixed loan if possible. Even though your home may never be paid off in your lifetime, your payments will be lower. Since you will be living on a fixed income, it is important that your payments stay as low as possible and do not change.

If you are a first time home owner, get the shortest term fixed mortgage possible. The rates are typically lower for 10 and 15 year mortgages, and you will build equity in your home sooner. If https://www.politico.com/newsletters/weekly-agriculture/2021/06/01/agriculture-in-bidens-budget-request-795647 need to sell you home and purchase a larger one, you will have more cash to work with.

Think about your job security before you think about buying a home. If you sign a mortgage contract you are held to those terms, regardless of the changes that may occur when it comes to your job. For example, if you are laid off, you mortgage will not decrease accordingly, so be sure that you are secure where you are first.

Be sure you understand all fees and costs related to any mortgage agreement you are considering. Make certain all commission fees, closing costs and other charges are itemized. linked web-site can often negotiate these fees with either the lender or the seller.

Don't take out a mortgage for the maximum amount the bank will lend you. This was a strategy that backfired on thousands of people a few short years ago. They assumed housing values would inevitably rise and that payment would seem small in comparison. Make out a budget, and leave yourself plenty of breathing room for unexpected expenses.

Remember that it takes time to get a mortgage closed; therefore, it is important to include enough time in the sales contract for the loan to close. Although it may be tempting to say the deal will be closed within 30 days, it is best to use a 60 or 90 day timeframe.

During your application for a home loan, get a rate-lock. A rate-lock in writing guarantees certain terms and interest rates for a given period of time. Set the rate-lock "on application" instead of "on approval". The lock-in period needs to be long enough to allow for factors that can delay the loan process.

Do not get confused with wording. Many people do not understand the difference between loans that are pre-approved or pre-qualified. When you are pre-approved a lender is potentially offering you the funds. When you are pre-qualified you are not being offered funds. Instead they are offering you a chance to become pre-approved.

All loans carry risk. You really must get a loan that suits your family's needs. This information has given you what you need to make a good decision.